Property storm damage can turn your world upside down. Amid the chaos, navigating the intricate insurance claims process to get your property owner insurance settlement check and restore your property to its former glory can seem daunting.

In this comprehensive guide, learn how to navigate the property damage insurance claims process and get ahead of any obstacles you might face.

Property restoration contractors, public adjusters, and attorneys: Be sure to share this with your property owners.

What You Need To Know Before Filing Your Property (Home) Insurance Claim

The claims process can be overwhelming for a lot of people, but knowing what to expect can help you feel more at peace with the process. Here are a few key details you need to know before starting the claims process.

You’ll work with multiple claims adjusters.

Commonly, there’s a field adjuster and a desk adjuster. A field adjuster is an adjuster who comes to your home to assess the damage on the insurance company's behalf. However, most of the time, you’ll speak to the desk adjuster. The desk adjuster is the person who handles your claim from start to finish.

Your field adjuster doesn’t have access to your policy information.

They're strictly there to assess your property’s storm damage. If you have questions about your coverage, you’ll need to call your desk adjuster.

You should involve your contractor in the field inspection process.

Because your contractor is the first person to assess the storm damage, they can be helpful during the field inspection process. What they can offer is the ability to point specifics out to the adjuster and help answer questions you might have after the inspection is complete.

You’re responsible for paying the contractor’s deductible.

Your property owner settlement check is typically written for the actual cash value (ACV), which is the cost of the repairs or replacement minus wear and tear and the deductible.

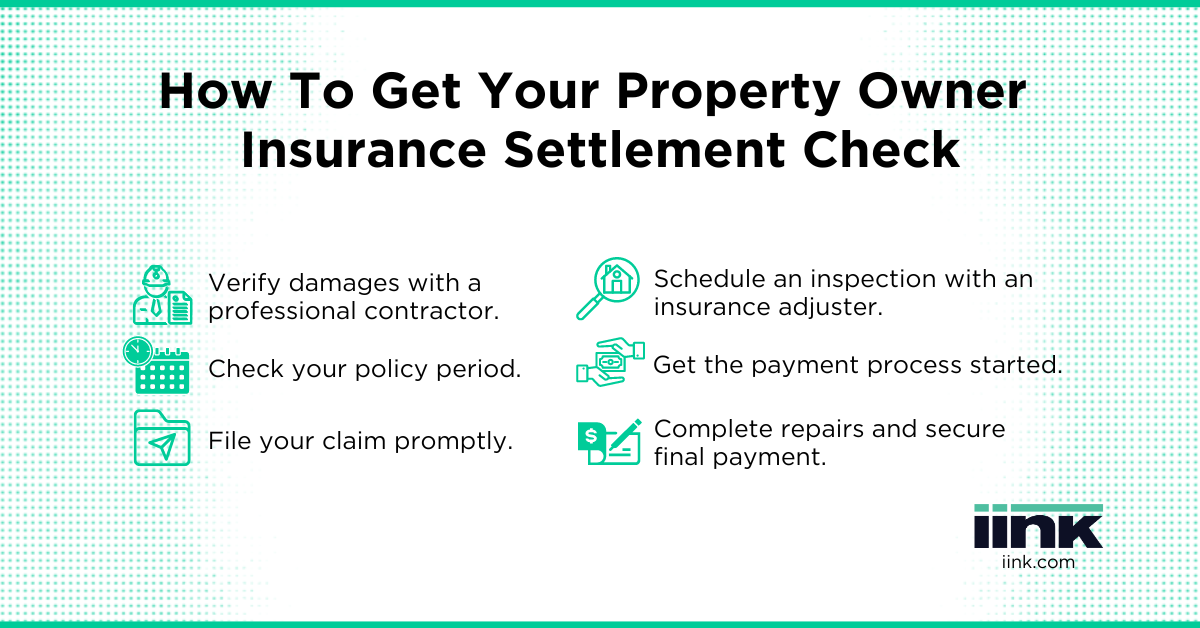

Step-by-Step Guide: How To Get Your Property Owner Insurance Settlement Check

When you file a claim for storm damage to your home, it’s important to follow the claims process completely. You don’t want to skip any steps or miss any deadlines because doing so could cause the insurance company to deny your claim altogether.

While the process can vary slightly between carriers, here are the basic claims process steps to follow to help secure your property owner insurance settlement check.

Step 1: Verify damages with a professional contractor.

If you believe your home was damaged during a storm, you should first consult a professional property restoration contractor to verify the damage. Make sure the contractor you choose is reputable, licensed, and insured.

It’s important to have a contractor assess the damage immediately so you have the date of loss documented accurately.

Step 2: Check your policy period.

Property and homeowner policies are valid for one year at a time. Review your policy to ensure coverage is valid. The damages you’re claiming may need to fall within the one year period to qualify.

Step 3: File your claim promptly.

As soon as the contractor assesses your storm damage, file a claim with your home insurance carrier to start the process. Insurance companies require you to file claims within a specific period of time.

For most home insurance policies, you must file your claim within one year of the date of loss. However, this varies by carrier, so it’s important to know your policy’s restrictions and start the claims process as soon as possible.

Step 4: Schedule an inspection with an insurance adjuster.

Once the claim has been filed, arrange a field inspection with the insurance adjuster. The field adjuster, often a subcontractor for your insurance company, acts as the eyes and ears for the desk adjuster. The desk adjuster is the adjuster who handles your claim from start to finish and issues your final payment.

Step 5: Get the payment process started.

Once the desk adjuster has received the inspection report from the field adjuster, they will then review the policy to determine that the damages are covered during your policy period.

The insurance company will normally pay you in two checks: the first check (actual cash value - ACV) and the second check (replacement cost value - RCV) are normally paid once the work has been completed and the insurance company has received the certificate of completion and the deductible has been paid to the contactor.

Step 6: Complete repairs and secure final payment.

After the contractor completes the work, provide proof to the desk adjuster to approve the final payment. This can include photos of the completed work, a letter of satisfaction, or a certificate of completion from the contractor.

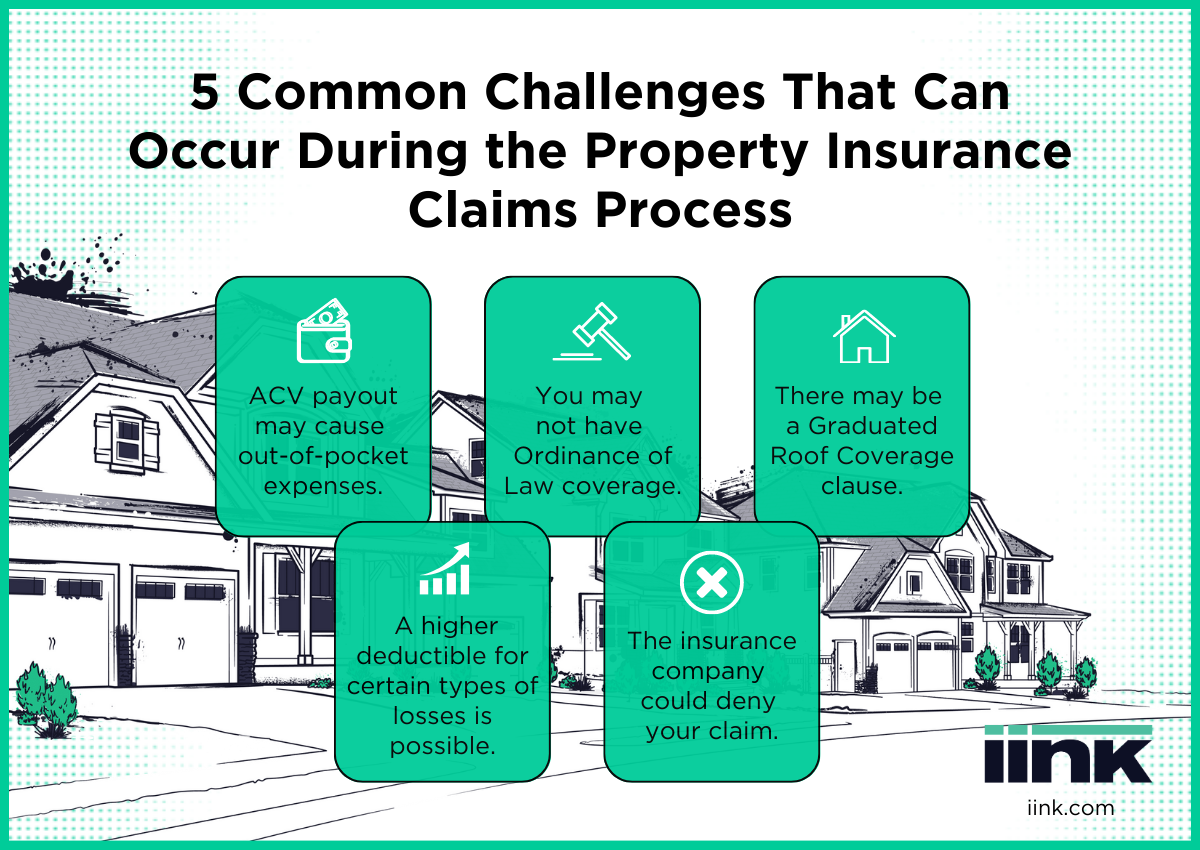

5 Common Challenges That Can Occur During the Property/Home Insurance Claims Process

The claims process isn’t always straightforward. You might face some challenges, but don’t worry—there are always ways to overcome them.

1. ACV payout may cause out-of-pocket expenses.

Your home insurance policy is a contract. It lays out, in detail, what’s covered and what’s not covered. But it isn’t always easy for many insured property owners to understand where coverage is limited.

Most policies pay claims using the ACV calculation and as a result, the total cost of repairs or replacement isn’t always what’s paid out. Instead, the insurance company subtracts the cost of wear and tear and your deductible to determine the payout.

Unfortunately, this means to get your home fixed, you could have some out-of-pocket expenses.

2. You may not have Ordinance of Law coverage.

Ordinance of Law coverage pays for any upgrades needed due to new building codes being put in place.

For example, if your home was built in 1970 and wasn’t updated for every building code change since then, repairing storm damage so that your home is up to current building codes will cost more.

So if you don’t have Ordinance of Law coverage, there’s a gap in your coverage that results in higher out-of-pocket costs.

3. There may be a Graduated Roof Coverage clause.

If your policy has a Graduate Roof Coverage clause, it limits the amount the insurance company pays for roof claims depending on the age of your roof. So the older your roof is, the less the insurance company covers.

Because of this, if you have a roof claim, your insurance company might not pay to replace the entire roof. You’d have to pay a portion of the cost plus your deductible.

4. A higher deductible for certain types of losses is possible.

Certain types of losses have higher deductible amounts. This could be a problem because you’re responsible for paying the deductible. For example, in Florida, hurricane deductibles are a percentage of your dwelling cost – typically between 1% and 5%. So if a hurricane caused damage to your home, you’d pay more out of pocket than your standard deductible.

Coverage-specific deductibles vary by state. This is why it’s important to review your policy to see what perils are covered and how the coverage works.

5. The insurance company could deny your claim.

An insurance company could deny a claim entirely. However, if this happens, there’s a dispute process you can follow. Simply let your adjuster know you are disputing their denial and requesting a second inspection. You might also want to consult with a lawyer to help you through the denial process.

The Solution: What To Do If You’re Responsible for Some Property Restoration Costs

If you’re responsible for some of the repair costs, don’t panic. Alternative financing options are available.*

Gap financing through our partnership with Momnt, covers the difference between what your insurance company pays and the repair costs. And it’ll even help you pay your deductible.*

Apply for gap financing here or contact our sales team for additional information.

*Subject to approval