When it comes to property insurance claims, navigating the payment process can sometimes feel like deciphering a complex puzzle. Each claim is unique, and so are the payments associated with them. Understanding this process is key for a efficient property restoration. Let's dive into the nitty gritty of the property insurance claim payment journey.

Types of Payments Related to Property Claims

1. Actual Cash Value (ACV) Payment. This represents the estimated value of the damaged property at the time of the loss. Determined based on fair market value, it considers factors such as age depreciation and condition assessed by the insurance company's adjusters.

2. Depreciation Payment. The difference between the Replacement Cost Value (RCV) and the ACV payment, along with the deductible. This payment is typically made upon completion of repairs or when the insured provides proof of deductible payment.

3. Supplemental Payment. Issued when the initial assessment underestimates the extent of repairs needed. Contractors provide evidence of additional work, leading to adjustments in the payout.

4. Deductible Payment. The responsibility of the insured, payable to the contractor. Deductibles can vary based on policy coverage.

5. Upgrades or Work Not Covered by Insurance. Any additional work beyond insurance coverage is borne by the insured. This includes material upgrades, extra labor requests, or additional services not related to repairs.

6. Settlement Award. A lump sum payment issued by the insurance company upon resolving disputes over coverage.

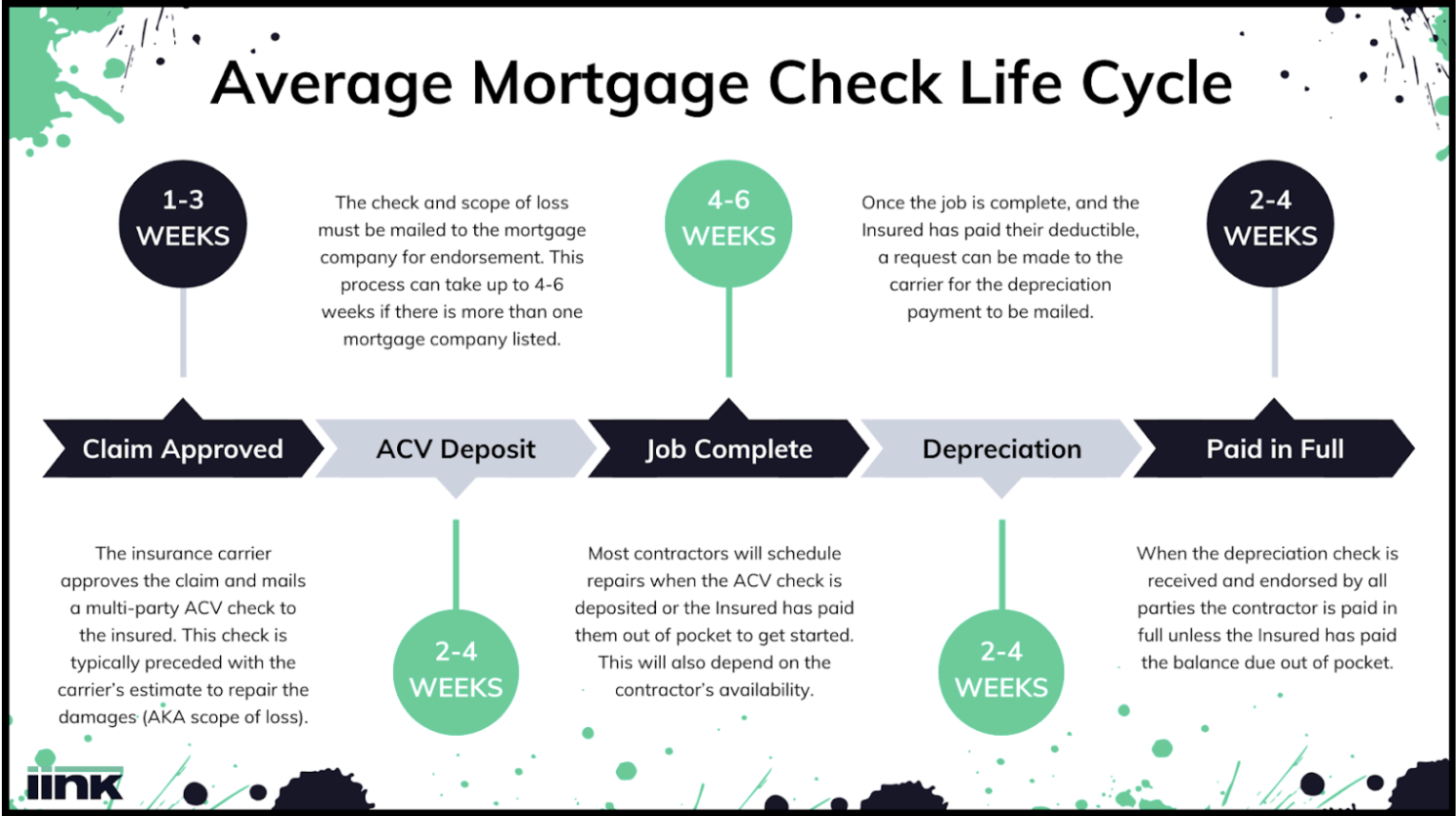

Average Turnaround Times for a Typical Roof Claim

From claim approval to final payment, the timeline varies based on factors such as check endorsement, bank processing, scheduling repairs, and completion of inspections.

What Causes Payment Delays?

Mortgage companies, dispute resolutions, and administrative processes contribute to extended payment timelines. Knowing these factors allow for better preparation and management of expectations.

- 64% of residential claims will have a mortgage company on the check.

- 11.6% of residential claims will have multiple mortgage companies on the check.

- 4% of checks with a mortgage company will be monitored due to account delinquency.

- 20% of checks with a mortgage company will be monitored due to total value of the loss.

- Checks may need to be reissued because they have the wrong mortgage company listed on it as a payee.

- Checks can get lost in the mail because they were sent without tracking.

- Checks can expire while securing all the necessary endorsements for deposit.

- Bank requirements and holds sometimes come up due to multiple parties being listed on checks.

Mortgage Company Guidelines

Mortgage servicing companies are responsible for managing loan repayments and are listed as payees on property loss checks so they can monitor the repairs of the investor’s (FannieMae, FreddieMac) collateral (the property). In short, they want to ensure the property is brought back to pre-loss condition. The mortgage company’s loss draft department is responsible for managing property claim payments. A vast majority of mortgage companies outsource their loss draft servicing to a third-party provider.

Non-Monitored Claims

- Under $40K RCV and

- No mortgage delinquency or assistance within 2 years of the date of loss

- Only need to verify insurance adjuster’s worksheet (scope of loss)

- Will typically stamp/endorse and release the check back to the insured

Monitored Claims

- Over $40K RCV or

- Mortgage delinquency or assistance within 2 years of the date of loss

- Will need adjuster’s worksheet, contractor agreement, waiver of lien, and possibly additional documentation depending on investor guidelines.

- Will perform progress inspections during the restoration process and a final inspection when complete. These are typically ordered and performed by a third-party and will add 1-3 weeks to each disbursement required. Disbursements are typically made at 50/90/100% completion, 40/30/30% completion, or similar depending on investor guidelines.

Best Practices for Streamlined A/R with Insurance Jobs

Best practices to help streamline the accounts receivable process includes:

- An SOP is a must. Have a standard operating procedure (SOP) for your account’s receivable process. Make sure everyone in the company is familiar with it and understands how the process is supposed to go.

- Customer education. Educate your customers on the property claim payment process before the claim is approved so they are prepared for it when the check arrives. If they don’t know what to do, it can cause unnecessary frustration and delays in getting paid.

- Get documents distributed ASAP. Provide the insurance company’s claim department with a copy of your contract, a direction of payment request with claim number and property address signed by the Insured, and your company W-9 as soon as possible. This will increase their likelihood of the carrier adding your company name to the approved claim check(s).

- Keep records. Save contact information, mailing addresses, documents, and process instructions for each mortgage company. Make sure to periodically verify the information as mortgage companies will sometimes change locations, revise processes, get acquired, etc.

- A third-party letter of authorization is a must. Make sure to get an appropriate third-party letter of authorization signed by the borrower (insured) so that you may speak with the mortgage company when necessary about the check disbursements.

- Follow up. Follow up with the mortgage company 3-5 days after they’ve received each check to ensure they have everything necessary to endorse and disburse the check. If they’re missing a document, for example, you’ll find out sooner than later and keep the process moving forward.

- Even more record keeping. Save all tracking information, copies of checks, and notes of your correspondence with all parties (particularly the mortgage company) throughout the endorsement process.

- Open communication. Keep all parties informed on the status of the check, especially its whereabouts. If you know the mortgage company mailed the check back, inform the insured so they know to be on the lookout.

- Be prepared to enforce your contract. Remember, your customer owes you payment for services rendered regardless of delays that might be outside of their control. Be prepared to enforce your contract with the proper disclosures and a mechanic’s lien, if necessary.

- Maintain a healthy cash balance. You want to maintain 3-6 months of runway cash to cover operating expenses during insurance restoration payment processing. Just because “the check’s in the mail” doesn’t mean laborers, materials suppliers, company staff, landlords and utilities providers will wait for payment. Don’t rob Peter to pay Paul!

As you now know, navigating the property insurance claim payment process requires diligence, understanding, and effective communication. By familiarizing yourself with the intricacies of this process and implementing best practices, you can ensure timely payments and a smoother restoration journey for all parties involved. Additionally, if you’d like to learn more about the foundations to build a strong financial process when it comes to insurance claims, make sure to check out our webinar: The Fundamentals of Financial Management in Public Adjusting.