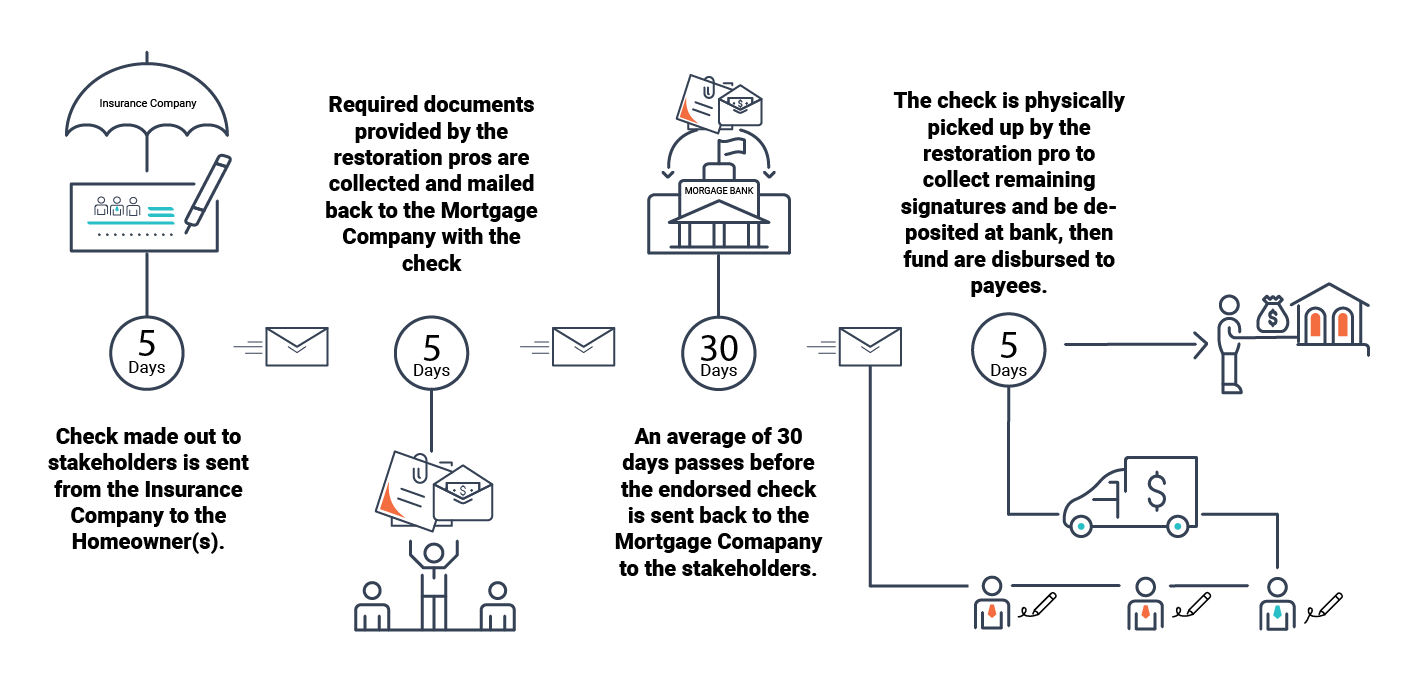

Suppose you’re a property restoration professional or an insured property owner dealing with a property claim. You may or may not be familiar with the frustrating process of actually receiving the funds to get property restorations done. Doing so starts with the insurance company issuing a multi-party check. Dealing with a paper check that has several payees listed is a hassle just by itself. Having the mortgage company listed on the pay to the order line makes this whole process take 30 to 45 days.

On average, the insurance companies will include mortgage companies on more than 60% of all property claim checks, and that will continue as long as paper checks are around. Additionally, about one out of every five claims will be “monitored” by the mortgage company. Property owners with a replacement cost value over $40,000, recent mortgage delinquency, or modification/forbearance within two years of the date of loss are in most cases considered as a monitored claim.

What happens if this is the case for you?

They will require additional paperwork, perform inspections through the restoration, and disburse funds based on their guidelines (typically, no more than 33% of the check to start).

Ultimately, this can lead to delays in repairs, unpaid invoices, and contractors utilizing limited company resources to float all the job expenses.

(The lack of cash flow is the number one cause of contracting businesses failing and attributes to over 60% of all contractors going out of business within the first five years.)

(For the Insured, it means being in disrepair or displaced from their home indefinitely.)

Is the mortgage company listed on the check? Here are some tips that will help you navigate the mortgage loss draft process without pulling your hair out (or worse). Contractors keep in mind that running a successful accounts receivable department will depend on many other factors.

(Restoration professionals assisting with the claim or performing repairs will consider implementing these five strategies to keep their cash flow moving.)

1. Have A Standardized A/R Process in Place

If you don’t have one already, there is no better time than now to implement a standardized accounts receivable process. Start documenting every customer payment scenario from start to finish, including who collects what, when they collect it, what they do with it, why they that way, etc. Please make sure EVERYONE in the organization is aware of the process and held accountable for it. Every company does things a little differently, and that’s OK. But, once you identify an effective A/R method that works for your type of organization/industry, execute it across the board and only adjust as necessary.

2. Educate Your Customers Ahead Of Time

It’s generally best to educate your customers up-front on what to expect throughout the entire claims and restoration process. That way, you can avoid unnecessary issues like issuing checks by the insurance company with the incorrect mortgage companies on them. This is usually because the mortgage was refinanced or sold, and the Insured didn’t update the mortgagee clause in their policy. If the mortgage originator (a company that got the loan for the person buying a property) was listed on the policy when the property was purchased but the loan got sold to the mortgage servicer (a company that handles payments and services the loan payments), then the check would need to be issued with the mortgage servicer name instead of as a payee. The time-consuming problem of having a check reissued can be avoided by simply letting your customer know to verify the mortgagee clause in their policy before their claim is approved. If the mortgage company listed is incorrect, the Insured can correct it with their agent (not adjuster), and their claim check will be issued with the right mortgage company.

3. Provide Customer Service Whenever Possible

Taking care of the check processing for your customer may feel like “one extra thing to do,” but the reality is that you can manage your receivables this way more effectively. You are leaving it up to an Insured who’s just experienced a property loss and probably never had to deal with this before may not yield the best results. They rely on the expertise of their claims professional, and so should you when it comes to getting paid for your work (hint hint). If you don’t have the time or resources to help the insured with their claim check, then a little professional guidance will go a long way if you have the time and resources to do the lost draft. In that case, you can expect to get paid in a more timely fashion, see contract retention rates increase, and probably get more referrals to deliver a positive customer experience. Just don’t forget to have your customer sign a third-party letter of authorization for you to speak with their mortgage company on their behalf.

4. Over-Communicate to the Mortgage Company

Regardless of who’s handling the correspondence with the mortgage company, details must be confirmed and statuses followed upon. Don’t just mail the insurance check to the mortgage company where the monthly payment usually is sent. Call them first and speak to the loss draft department for details on where to send the check, if it should be endorsed or not, what documents are required, if they have email/fax to send those documents, how long the verification/return process will take, and where they will send the check when it’s sent back—document everything. Follow up with the same department to confirm the check was sent back when they said it was going to be sent. If not, ask why and remind them that work either has to commence or has been completed. Escalate to management if things seem to be going nowhere or you’re getting the runaround.

5. Track Results and Stay Efficient

Knowing what you’re getting into before engaging a mortgage company will help keep the process moving as quickly as possible. Even though government-sponsored enterprises like FannieMae and FreddieMac put forth loss draft guidelines for mortgage companies to follow, they sometimes get left up to interpretation or don’t apply to every loan scenario (don’t assume anything). Keep track of various mortgage company timelines, individual practices outside the norm, and management contact info if you ever get a hold of someone at that level (you never know when you’ll need it again). Fax or email required docs to loss-draft whenever possible and then mail the check using 2-day service with tracking. Provide a return label for the insurance claim check to be sent back to your office (they won’t always use it at least you tried). Finally, please don’t waste money overnighting the claim check(s) either because it will still take a couple of days for the documentation to get into the mortgage company’s system.

Property restoration is a process that involves more than just hammers and nails. Own as much of the process as you can, from start to finish, and you’ll set yourself ahead of the competition by delivering exceptional service. Remember, your customer has experienced damages to their home or business, and they’re trusting you to help them get back to normal. Give them a positive experience all around, and you’ll capture more raving fans on your way up the ladder of success.